New York City clearly has a housing emergency. The dire shortage of housing has created a market which overwhelmingly benefits existing landlords and property owners, by exacerbating demand at the expense of renters. As discussed in an earlier post, New York City averages a 3.12% rental vacancy rate, which is well below a minimum 5% vacancy rate needed to ensure adequate access to quality, affordable housing. A healthy vacancy rate is important as it helps to buffer against high rents, helps increase access to a variety of housing types, and encourages competition and individual consumer choice in the housing marketplace.

However it is no small task to increase the city’s vacancy rate. In order to reach a minimum 5% vacancy rate by 2025, it would necessitate the creation of 27,000 new rental units per year for the next 12 years. This is something that neither the private market nor government can do alone. Here are just a few examples of how the city could increase the vacancy rate and augment the stock of affordable housing…

I. REDEFINE AFFORDABILITY

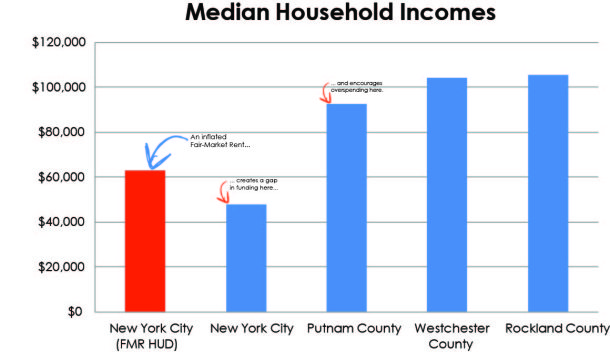

There are currently three different sets of median annual household income for the New York City metro employed by HPD, the US Census, and US HUD, ranging from $48,040, $51,270, and $63,000, respectively. Unfortunately, the NY HUD Metro FMR Area Median Income (AMI) rates, which are used to determine housing affordability (and therefore federal and state financing), include all five New York City boroughs as well as Rockland, Putnam and Westchester counties.

Due to federal statute 42 USC §1437a, Westchester and Rockland counties are included in the NYC Metro but must determine their income limits individually. However Putnam County is still included in the broader metro area. Not only does this over-inflate the income levels for New York City, but Putnam County is able to utilize skewed income limits for their affordable housing projects as well. Individually, HUD limits for Rockland and Westchester are $105,400 and $104,200, respectively. Putnam’s limit is set the same as NYC but their US Census median household income is $92,711; New York County’s median income is only $67,204 by comparison.

Redefining affordability will help allocate housing funds more efficiently to those who need it most, while ensuring a more equitable regional distribution among affordable housing providers (federal and state distribution of CDBG, HOME funds, etc.). By reducing the city’s HUD income limits, more housing development projects will become accessible to a wider set of the population and encourage more cost-effective, lower-income developments rather than wasting valuable resources in expensive, high-income counties. While some middle-income earners may become ineligible in New York City (the limits would be reduced if Putnam left the equation), the increase in rental vacancy rates related to other programs may help reduce the need for subsidized middle-income housing.

Focus on renters rather than homebuyers

Many of the city’s affordable housing programs do not currently differentiate between qualifying AMI’s of potential renters as compared with potential homebuyers, even though median household incomes, and therefore their housing support need, is extremely different. For example, the median household income for a renter in the city is $38,500 while the median household income for a homeowner is $75,000.

In order to provide cost-effective distribution of affordable housing funds, funding levels should more closely resemble the fact that the city’s homeowners earn almost double that of renters. Affordable condos, co-ops, and other home-ownership projects should be required to meet deeper affordability rates in order to qualify for funding. Ultimately, this will allow more funds to be available for a greater number of affordable rental housing initiatives as hard-to-reach rental support is often less expensive. Besides down-payment assistance, most affordable home-ownership programs are an outdated relic and stretches valuable resources in a renter-dominated NYC.

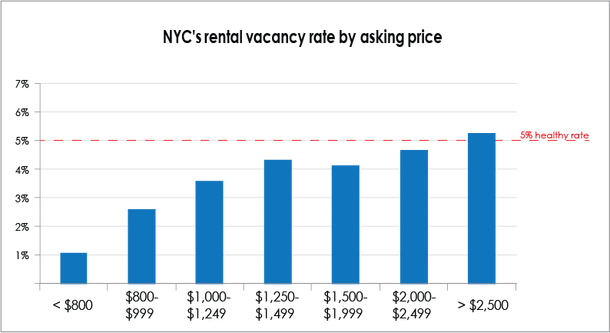

What the above chart shows us is that we may not really need a drastic increase of rental units charging more than $2,000 per month. Any affordable housing recommendations should therefore focus on increasing the number of units available in the lower price brackets. By funding less-expensive units, the City can construct more units overall.

As well, the New York City Housing Trust Fund (HTF), which is no longer in operation, could be reinstated to help fund new construction, major rehabilitations, land acquisitions, and preservation of citywide affordable housing. Funds garnered from new programs, discussed later, would be set aside specifically for households earning less than 80% of a newly redefined AMI.

- Reduce AMI Rates: Provide greater access to deeper affordability rates for the city’s population most in need.

- Greater funding for rentals: Redefine AMI levels to account for the discrepancy in renter and homeowner median household incomes and to prioritize hard-to-reach renters.

- New York City HTF: re-establish the affordable housing trust fund which would be used to fund new construction, major rehabilitation, land acquisition, and preservation of citywide affordable housing.

II. MODERNIZE ZONING

In New York City, there are approximately 8,000 acres of residential land zoned R5D or less (<2.0 FAR, ~1-3 family homes) within ¼ mile of a subway station. Just to give an example, an overall increase of just 0.5 FAR of these areas could potentially create over 146,000 new units of housing at an average of 1,200sf per unit. By focusing on existing low-density areas well-served by mass-transit, the city could easily increase the supply of housing within the private market and act as a “pressure-release valve” on the dire vacancy rate. Further density increases could be considered along wide-streets, coupled with enhanced commercial overlays, to create higher-density corridors utilizing the existing Inclusionary Housing (IH) bonus program, which provides full utilization of a density bonus for provision of affordable housing.

A citywide initiative, in partnership with existing local development corporations (LDC’s), could further study LDC-selected opportunity corridors in the neighborhoods of Canarsie, Ocean Parkway, Gravesend, Bay Ridge, Windsor Terrace, East New York, Cypress Hills, Ridgewood, Woodside, Elmhurst, North Corona, Astoria, Jamaica, Kingsbridge, Unionport, and Pelham Parkway. These areas could be designated as priority receiving areas for city and state affordable housing funds and implement a strengthened Inclusionary Housing program.

Since these geographies must rely heavily on efficient mass-transit to jobs and services across the city, housing developers could have a menu of options in order to receive a given Inclusionary Housing density bonus. These could include adding funds to the HTF, increasing their payment into the MTA’s portion of the real property transfer tax, and/or paying into a Transit Expansion Fund (TEF) which would act as a dedicated source of investment for service improvements in the designated growth areas mentioned above. Parking requirements should be reduced or waived altogether.

- Upzone Transit Corridors: new development rights and reduced parking requirements could result in an additional 7,000 market-rate units per year.

- Strengthen Inclusionary Housing: increased FAR penalty for not utilizing IH in designated areas and boosted IH requirements could result in an additional 3,000 units of affordable housing per year.

- Menu of funding: determine and implement a menu of payment opportunities for developers citywide to pay into the HTF, an increased RE transfer tax, payment into a TEF, or a combination of these payments.

III. GET VACANCIES WORKING AGAIN

Annually, there are approximately 110,000 vacant units unavailable to sell or rent in New York City. 40% of these units are used only occasionally as seasonal or recreational homes while another 30% are undergoing or awaiting renovations. It may be feasible to increase the tax rate on seasonal or recreational residential units in the city, with the hope that some will be pushed back into the market, with the new source of revenue dedicated to the HTF. As well, the city could initiate a Rapid Repair & Renovation (RRR) program, geared specifically for renovations of units available to residents below 150% AMI. RRR would help speed permitting and inspection process, and could connect renovation projects with special access to renovation loans.

In New York City, which has a dearth of developable land, property owners should not be encouraged to keep residential properties vacant by means of lower tax assessments. To further increase the supply of new homes, a new, higher tax rate could be placed on vacant residential land to encourage its redevelopment. All new tax proceeds on vacant residential land could be dedicated for the HTF. On a tangential note, vacant industrial and heavy commercial parcels could be studied to understand the impacts of a higher-tax rate, in order to prevent land-banking of these properties in hopes of future residential rezonings.

- Recreational Home Tax: pushes 2,000 market-rate units into the market per year and could produce an additional $44 million in tax revenue annually (estimates a 10% decrease in recreational homes. Increase in quarterly tax rate of 0.0125%. Would equate to an additional $1,000 per year for recreational homes with an assessed value of $2 million).

- RRR Program: potentially pushes 2,000 affordable-units and another 4,000 market-rate units into the market faster, every year, with minimal cost.

- Vacant Lot Tax: re-categorize vacant residential land to a higher-rate tax class, which could increase tax revenues from 6% to 45%. This has the potential to create 5,000 new units, 2,000 affordable, per year (there are more than 30 million sf of vacant land zoned R6 or greater. Unit count assumes only 20% of that is developed, and at an average of 4.0 FAR).

IV. REDUCE THE COST OF DEVELOPMENT

New York City experiences the highest development soft- and hard-costs of any city in the United States. Unfortunately, these high costs are often passed on to tenants through increased rents. Materials, labor, and permits are just a few of the costs that the city could help reduce in order to increase housing access and affordability. The City could develop a Fast-track Archetype & Vendor Redevelopment (FAVR) program. This program has two major components:

- Develop and maintain a series of residential “archetypes”; and

- Develop and maintain a dedicated vendor pre-fabrication program.

Archetypes

In the short-term, a panel of city agency representatives, stakeholders, and community representatives could hold an intensive design competition in order to model a series of residential development archetypes or typologies (this is inspired by architect and former member of the City Planning Commission Stuart Pertz’s concept for a NYC rowhouse archetype) to be approved by each Community Board. These could include high-quality row-houses and apartment buildings well-suited to the proposed outer-borough housing expansion, and could provide an opportunity for cohesive placemaking unseen since the Brownstone boom of Central Brooklyn in the late 19th century.

Once the archetypes are publicly selected, the NYC Department of Buildings (DOB) could provide the site-plans and blueprints free-of-charge to developers, and could further allow automatic as-of-right development within specific zoning districts. City agencies’ familiarity with the designs would help reduce the time and costs associated with permitting, which would in-turn, need little pre-development review. This could also reduce the soft-costs associated with developers’ legal teams, expediters, and architects, among others, creating a virtual fast-track for development.

Fabrication

There is also demand-side benefits associated with a formalized and consistent housing typology: pre-fabrication opportunities. Beyond regulations, permitting fees, and fines, labor and materials are some of the highest costs associated with NYC’s housing development. Off-site pre-fabrication of materials has proven an effective way to reduce costs and waste. New York City has not only been able to capitalize on this, but has also found pre-fabrication a way to bring new, high-paying manufacturing jobs back to the city (Capsys Corporation, a modular home fabricator based in the Brooklyn Navy Yard, has already constructed 2,000 new units for developments across New York City and the country).

The second facet of the FAVR program is to develop an approved vendor program. Through a rolling bid process, publicly incentivized vendors (located in Industrial Business Zones, minority and women-owned businesses, employee wage requirements, proximate distance to a project, etc.), working in conjunction with the NYC Economic Development Corporation and Small Business Services, could begin to efficiently pre-fabricate the materials based on the official DOB archetype plans. The resultant consistency of bulk production could further reduce construction costs while increasing local manufacturing jobs.

The City and State could also recommend the reduction or waiver of sales tax on residential building materials purchased through the FAVR program. Another source of revenue could call for a portion of all city sales tax generated from residential construction materials, regardless of participation in the FAVR program, to be dedicated to the HTF.

To further reduce housing costs, tax assessments on new construction with affordable housing could be waived out of ULURP, CEQR, and other permitting process fees, as it inflates the assessed construction costs over the life of the development. All fees and permits could be subtracted from affordable housing assessments.

- FAVR Program: develops and maintains a series of housing archetypes and dedicated vendor program to speed up quality housing production and reduce development costs. This has the potential to create an additional 4,000 units into the market per year.

Trackbacks/Pingbacks

[…] How to end the NYC housing emergency (Part 2) […]

LikeLike this